Investment portfolio perspective modeling

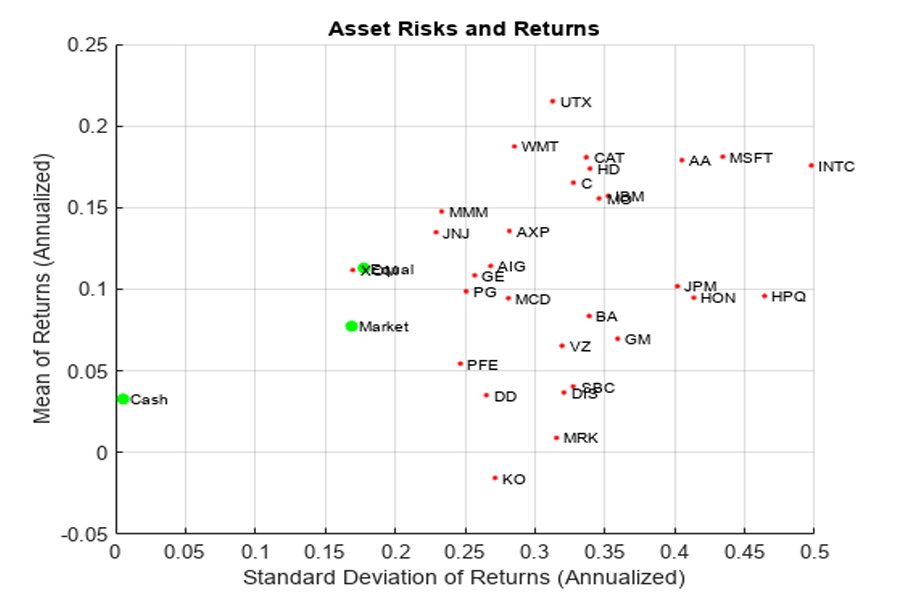

Making investment decisions requires intricate mathematics in order to reduce risk. We look into portfolio optimization, which is a branch of economic and financial modeling that aims to maximize the expected return on an investment.

We investigate a linear programming approach to developing a decision model for a first-time investor. Our outcomes are computed based on adjusting our models used for calculating rates of return and failure rates in order to best capture reality.

Portfolio Optimization

A mathematical approach to aid in making the decision of what mix of assets to invest in, according to certain criteria

We then investigate how changing our constraint of confidence in our investment affects the model's distribution.